Harmonizing national rules and standards can encourage mobility and improve the efficiency of the labor market.

- By

- February 26, 2016

- CBR - Economics

Harmonizing national rules and standards can encourage mobility and improve the efficiency of the labor market.

A version of this article appeared on Voxeu.org on December 17, 2015.

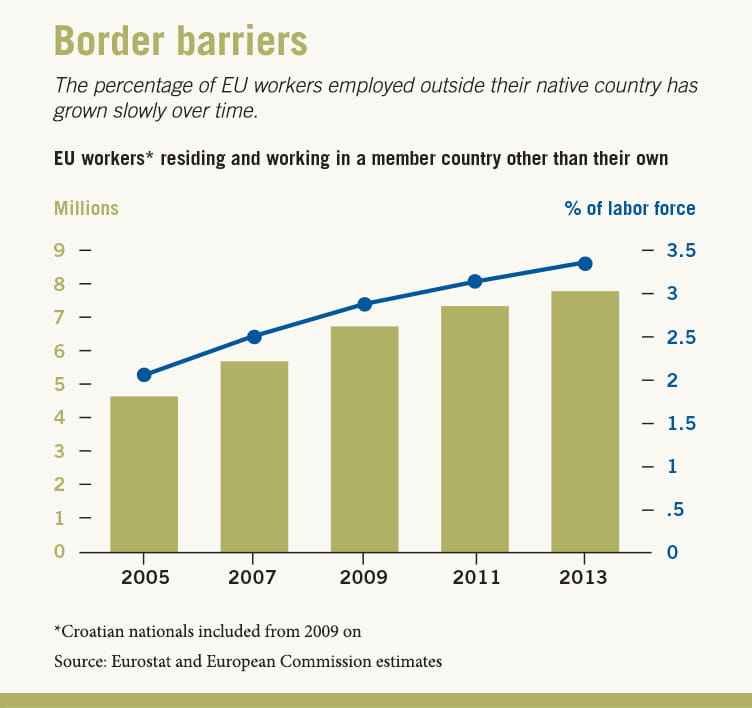

The 1993 Maastricht Treaty, which formally established the European Union, set out to achieve “four freedoms”: the free movement of goods, services, people, and money across the continent. But more than 20 years later, there’s still relatively little movement of people, and in particular of workers. Some 7 million EU citizens are working and living in a member country other than their country of citizenship, according to László Andor, former commissioner for Employment, Social Affairs, and Inclusion in the European Commission, while another 1.1 million cross-border workers are employed in one country and live in another. While the numbers may sound impressive, the 7 million “mobile workers” account for only about 3.3 percent of the EU’s total labor force.

Labor mobility clearly plays an important role in the efficiency of labor markets. It can, among other things, help regions adjust to asymmetric economic shocks, especially in a currency union such as the eurozone. Recognizing the importance of labor mobility, the EU has taken various steps in recent years to increase it, by harmonizing social-security policies and providing ways for citizens from one EU country to have their foreign professional qualifications recognized in another. Such efforts can reduce the costs of migration, according to Martin Kahanec, of the Central European University in Budapest. However, many professional rules and standards remain national—and for a professional, having to meet national standards likely makes it difficult to migrate across borders. The existence of different national standards therefore constitutes an implicit economic barrier.

The accounting profession is an interesting case in this regard. Over the past decade, national accounting and auditing standards have to a large extent been replaced by international standards now common across the EU member states. This change provides us with an opportunity to study the extent to which professional standards constitute an economically significant barrier to cross-border migration. It also allows us to examine whether harmonizing standards can have a meaningful effect on cross-border mobility. If we find such an effect, that would suggest regulatory harmonization could be a potentially important policy lever to spur the migration of skilled labor and professionals.

Despite the potential importance of harmonization, its effect on cross-border labor mobility has been little studied. Much of the prior literature on labor migration has focused on the effects of wage and unemployment differentials, immigration laws, or occupational-licensing rules. The latter two are explicit, government-enforced rules that restrict who can move into a particular country or who can offer services in a market. The prior literature finds that such explicit restrictions create mobility barriers.

Our study in turn examines differences in national standards, and whether they can also create indirect and perhaps subtler barriers to cross-border mobility. The focus on labor mobility also distinguishes our research from the existing literature on harmonization of accounting standards, which focuses almost exclusively on informational effects in capital markets.

In our analysis, we examine how the recent EU harmonization of professional standards in accounting and auditing affected cross-border migration of accountants relative to other professionals and comparable workers. The accounting profession provides a powerful test bed for cross-border labor migration patterns because it generally has a much higher level of standardization than comparable occupations, and regulatory harmonization has taken the form of adopting identical rules or standards across EU countries. Both factors make it easier to detect any effect that harmonization might have on the migration of accountants. The EU also provides a good setting because in principle it allows professionals to move freely, so our analysis is not constrained by immigration policies.

Generally speaking, regulatory harmonization should make it easier for workers to move to another country—but it is not obvious how large the effect is, for several reasons. The benefits from harmonized standards could be too small relative to other costs involved in international migration to have a meaningful effect. It is conceivable that factors such as language and cultural differences swamp any effects of harmonization. Moreover, BI Norwegian Business School’s Erlend Kvaal and University of London’s Christopher Nobes provide evidence that local accounting practices often persist after countries formally harmonize their standards. These local accounting practices and traditions could continue to act as an implicit economic barrier after the formal harmonization of rules, in essence mitigating or perhaps even thwarting positive effects.

In the end, the magnitude of the harmonization’s effect is an empirical question. To estimate it, we use data based on the EU’s annual Labour Force Survey, which includes approximately 32.7 million individuals from 29 countries over the 2002–10 sample period. To identify the effects, we compare changes in the mobility of accounting professionals with changes in the mobility of control groups consisting of comparable professionals (e.g., lawyers).

We estimate the effects within country and year to account for any unrelated changes and shocks that could affect mobility, such as changes in economic growth, unemployment benefits, and national adjustments to survey methodology. We control for changes in the domestic job mobility of accountants and other professionals, to ensure that our results do not reflect increases in the demand for accounting services during the implementation of the rule changes. And we account for demographic characteristics known to influence migration—including gender, marital status, age, education level, and the presence of children. While the data set does not allow us to follow individuals through time, we can construct bins of individuals who share the same demographic characteristics and estimate the effects within each bin—to make sure the effects we record are not driven by changes in the composition of the survey sample through time. We also adopt a statistical treatment in which we match and compare the mobility of accountants who were affected by regulation with other professionals who were unaffected and have the exact same personal characteristics. We create these pairs for a preharmonization year, and for a year after the regulatory harmonization. All our tests produce similar results.

We find that the EU’s regulatory harmonization produced strong effects. After accounting and auditing standards were harmonized, there was a 17–24 percent increase in the movement of accountants relative to comparable professions. This percent increase implies that the total effect on migration was equal to about 11,000–13,000 accountants. We also observe significant mobility effects when we limit the analysis to the EU-15 countries, for which cross-border mobility has been particularly low. Thus, while EU enlargement may play into the magnitude of the estimated effects, it is not the sole source of the mobility increase.

Overall, the results show that regulatory harmonization can have a meaningful effect on migration. Professional rules, when they differ from country to country, constitute a substantial barrier to cross-border mobility, consistent with the notion that the costs of learning and practicing other standards are economically significant. Recognizing this, policy makers could consider using the harmonization of national rules and standards as an instrument to encourage mobility and improve the efficiency of the labor market.

At Chicago Booth, Matthew J. Bloomfield is a PhD candidate in accounting, Hans B. Christensen is associate professor of accounting, and Christian Leuz is Joseph Sondheimer Professor of International Economics, Finance, and Accounting. Ulf Brüggemann is a postdoctoral scholar in accounting at Humboldt University Berlin.

Matthew J. Bloomfield, Ulf Brüggemann, Hans B. Christensen, and Christian Leuz, “The Effect of Regulatory Harmonization on Cross-border Labor Migration: Evidence from the Accounting Profession,” NBER working paper, December 2015.

Your Privacy

We want to demonstrate our commitment to your privacy. Please review Chicago Booth's privacy notice, which provides information explaining how and why we collect particular information when you visit our website.